Add-On Acquisitions are on the Rise

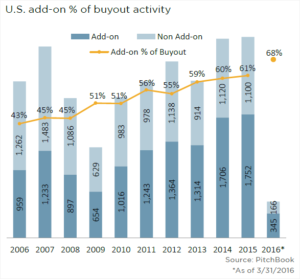

When developing an exit strategy for your company, we will consider whether Private Equity Groups (PEG’s) would want to acquire it as either a new platform company or as an add-on (also “bolt-on”) to one of their existing portfolio companies. Most small companies are too small or don’t have strong enough management teams to be attractive platform opportunities, however many are strong add-on candidates. According to PitchBook, which tracks the PEG M&A activity in the middle market, the number of add-ons as a percentage of all acquisitions grew from 43% in 2006 to over 60% in 2015 — and Q1 data showed a continuing increase to 68%.

What has caused this trend? A number of reasons are generally cited, including:

What has caused this trend? A number of reasons are generally cited, including:

- Larger companies typically trade at higher valuation multiples, and this gap has risen in recent years

- It has become increasingly harder to find good platform companies making add-ons more appealing

- Add-ons are easier to assimilate because the PEG already knows and understands the industry

- The increasingly shorter holding periods for platform companies makes a buy and build with add-ons a favored strategy

- An add-on can increase a platform company’s competitive position in its industry by providing synergies or access to a new niche market

- PEG’s can often use more debt to buy an add-on and invest less equity

As a potential seller of an add-on company, you might consider these questions, among others:

- How does your company align with and how could it be integrated into a platform company?

- In addition to a good strategic fit, PEG’s look for strong profit margins, a defensible market niche and revenue “stickiness”. Does your business have these qualities?

- Business continuity will be important to the buyer. Will you consider providing ongoing leadership and retaining some equity for a future sale at a potentially higher price per share?

- PEG due diligence can be exhaustive, as they are experienced and disciplined investors and typically require multiple approvals from lenders and investors. How will your company fare in such a deal environment?

If you are interested in understanding PEG investing activity in your industry and whether your company is a strong add-on or platform acquisition candidate, contact Jim Leonhard, CVA MBA at 916-800-2716 or jhleonhard@exitstrategiesgroup.com.

One of the critical documents used in the business sale process is the Confidential Information Memorandum or “CIM.” Other names for this document are pitchbook, deal book, offering memorandum and confidential business review. A CIM tells the target company’s story and lays out important facts and figures for prospective buyers. This article answers common questions about CIM’s and explains how they improve sale process outcomes.

One of the critical documents used in the business sale process is the Confidential Information Memorandum or “CIM.” Other names for this document are pitchbook, deal book, offering memorandum and confidential business review. A CIM tells the target company’s story and lays out important facts and figures for prospective buyers. This article answers common questions about CIM’s and explains how they improve sale process outcomes.