A Difference of Opinions: Closely-Held vs. Venture-Backed Companies- Part 1 of 2

In my transition from leading a valuation practice at an accounting firm to an M&A advisory firm, quickly realized significant differences between valuing venture-backed technology startups to valuing owner-operated small to middle-market businesses with between $2 million to $50 million in revenue. Over the last four years, I’ve concluded that there is a distinct and noticeable difference of opinions on the diligence, tools, and approaches used in valuing smaller, privately held companies. But before I dig into those differences, let’s define the fundamental difference between these two types of businesses:

- Venture-Backed Companies – These companies are usually startups based on an incredible idea that hopes to disrupt existing industries and markets. Some of the Companies I valued in their infancy include Tesla, Okta, Fanatics, and Uninterrupted. Some of these valuations were done before a Subject Company generated its first dollar of revenue and all were flying below the radar at the time of valuation.

- Privately-Held Companies – These companies include the companies that surround you every day from the local community market to the construction firm building homes in new developments to your local, downtown taproom. For me, they also include a growing number of owner-operated and family-owned craft beverage companies like wineries, craft breweries, distilleries, and cideries.

Now, let’s dig into the difference in how these different types of businesses are valued and how the type of diligence, tools, and valuation approaches used to value these various types of businesses differ significantly.

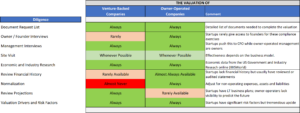

Exit Strategies Group prides itself on the platform and tools that it offers its appraisers and advisors for valuing companies for compliance, strategic, and M&A assessment purposes. In addition to our robust valuation model, we have a “Playbook” that is both a training and reference document that encompasses how we go about valuing and selling businesses. For this blog posting, I will only focus on the first two of these differences, diligence, and tools. Below is a “heat” matrix of how the differences I see in both:

Diligence:

All advisors have to follow strict guidelines regarding due diligence to meet compliance standards with the AICPA, USPAP, and other valuation standards. While the heat chart below shows differences between the diligence in valuing these two types of Subject Companies, they map to access to data and how a family business is managed differently than a venture-backed corporate startup.

Here are the biggest differences:

- Access – When valuing venture-backed companies, the appraiser is usually dealing with senior financial management during diligence. Rarely does a founder take on this role for a business. For owner-operated businesses, the conversations before engagement and through to a final report almost always include the founder or owner as the “key person” in charge of the business.

- Financial History – Venture-backed companies, by definition, lack any financial or operational history so it is almost impossible to analyze any trends over time. Owner-operated businesses usually have long histories that allow for this analysis.

- Financial Forecast – What a startup lacks in historical financial history they make up for with long-term forecasts that look at the growth of their target market, their share of that market, and ultimate profitability over time. Owner-operators rarely provide long-term forecasts and bemoan the lack of visibility in trying to plan more than a budget year ahead.

- Normalization – From the beginning, venture-backed companies are meant to be run in a corporate manner where senior managers (and founders) focus on their fiduciary responsibilities to shareholders. However, at times, there is an abuse of the policy of funds spent on “non-operating” or personal expenses. However, owner-operated companies are beholden to no one or have control of the business that allows them to run a business without a requirement for “market pricing” of everything from salaries and expenses. Therefore, it is almost always necessary to review the detail of an owner-operator’s financial statements to adjust for non-operating expenses, assets and liabilities, and above- or below-market salaries for themselves, and family members. The key question to ask in normalization is ”will a willing buyer need this expense or asset to run the business?”

Tools:

Similar to a carpenter who builds custom furniture compared to a construction worker building houses, valuation experts valuing these two types of businesses use different tools. The matrix below looks at some of these tools in greater detail.

Here are the biggest differences:

- Deal Databases – When valuing venture-backed companies, the appraiser ignores the comparison of the Subject Company with transactions completed in the industry in which it competes. The main reason is that a startup usually lacks specific comparables due to its business model and stage of development; they are at the beginning of its corporate life cycle while these transactions are “tombstones” for companies at the end of theirs. Owner-operated companies mirror the stage of development of these transactions. Therefore, this data is always used when valuing an owner-operated company.

- Publicly Traded Security Information – I have found that the approach to valuing venture-backed companies always relies on publicly traded market values and a guideline public company approach in valuing the business either at the Valuation Date or in the determination of a terminal value associated with a discounted cash flow (DCF). The simple assumption here is that if a venture-backed company is successful in its business plan and generating income, it will likely be publicly traded or compared to publicly traded companies at the end of a long-term (5-year) cash flow. Small, owner-operated businesses almost always lack that likely outcome. Therefore, while I always used this approach to value venture-backed businesses, I never use it to value

- Market Salary Adjustments – Unlike a venture-backed corporation that defaults to market salaries in its hiring process (even for its founders), owner-operated businesses see a wide range of the treatment of salaries in these businesses. I would say that I’ve seen an equal number of owners pay themselves above-market salaries as ones who pay themselves at below-market rates. Some don’t pay themselves at all. In this case, and as detailed above, we need to adjust for this policy to properly burden the Subject Company with market salaries to normalize the income statement for a willing buyer for them to properly value it. This assumption is at the heart of how we define fair market value.

In the coming weeks, we will look at the third of these differences, approach. It’s an important and detailed discussion that needs a separate blog post.

Exit Strategies values control and minority ownership interests of private businesses for tax, financial reporting, and strategic purposes. If you’d like help in this regard or have any related questions, you can reach Joe Orlando, ASA at 503-925-5510 or jorlando@exitstrategiesgroup.com.