Valuing Personal Goodwill

What is personal goodwill?

Before starting our discussion about personal goodwill, it is necessary to establish a common ground to understand the concept. First, it is an identifiable intangible asset that will generate future economic benefits to the asset owner. While there is no standard definition. Adam Mason and David Wood searched various textbooks, articles, and leading court cases[1]that define this term. From that exercise, we chose to utilize the following definitions for our discussion;

“Personal goodwill is the value of earnings or cash flow directly attributable to the individual’s characteristics or attributes.”[2]

“Personal goodwill, sometimes referred to as professional goodwill, is a function of the earnings from repeat business that will patronize the individual as opposed to the business, new consumers who will seek out the individual, and new referrals that will be made to the individual”.[3]

Personal goodwill differs from the concept of corporate or enterprise goodwill. Corporate goodwill is the simple calculation of the excess price paid for a company above the value of its tangible and identifiable intangible assets (i.e. brand, customer relationships). In some instances, goodwill can be negative, but that is the topic of another blog.

What is so relevant about personal goodwill?

In summary, it is a tax issue. In the sale of a C Corporation, an owner can have significant tax benefits when a portion of the purchase price is related to personal goodwill instead of corporate goodwill. This identification of goodwill as personal will allow the owner to avoid getting taxed twice for the same value. Let me explain. Assuming that all the goodwill is associated with the company, the sale would likely generate a tax at a corporate level before the after-tax value is allocated to the owners of the company’s stock. Once the owner receives the net proceeds, they would be taxed again at a personal level. Identifying a certain percentage of the goodwill as personal allows the owner to split the tax bill between personal goodwill and corporate goodwill and pay taxes on each only once.

Which characteristics or elements must have personal goodwill?

As with any other intangible asset[4], personal goodwill must have the following characteristics. It can be separated individually from the entity. In other words, if the business owner leaves her or his company, that intangible asset goes with them. For example, the ability of the business owner to generate sales because of its personal relationships. The other element to be recognized as personal goodwill is that the business owner has contractual or legal rights over that intangible asset. In that respect, the owner of the personal goodwill must not transfer it through an employment or a non-compete agreement.

How to estimate the fair value of personal goodwill?

We have found that the most logical and defendable way in which we estimate the value of personal goodwill is the “With and Without Approach.” This methodology consists in estimating the present value of the entity’s future cash flows as it is; that is, the “With” scenario. This “Without” scenario has several key inputs such as the impact the owner has on the company’s future revenues, the cost at which the company must replace the owner, and the time it takes to ramp the business up to its original “With” forecast. The difference in the value of these scenarios is the fair value of personal goodwill. An appraiser needs to provide strong support for some of these “qualitative” inputs, specifically the top-line impact of the owner. That diligence starts with a simple question to the owner as to his or her impact on sales as a % of the total and drills down to the detail of the revenues and the sales responsibility of each customer. An owner may suggest that the business would lose 50% of the revenue if he or she left but an analysis of the sales relationships with each customer may only suggest that impact to be 25%. In defending the “Without” scenario to the IRS, the more defendable number is always the right choice. The owner may disagree but the extra layer of support helps mitigate future audit risk.

What is the real impact?

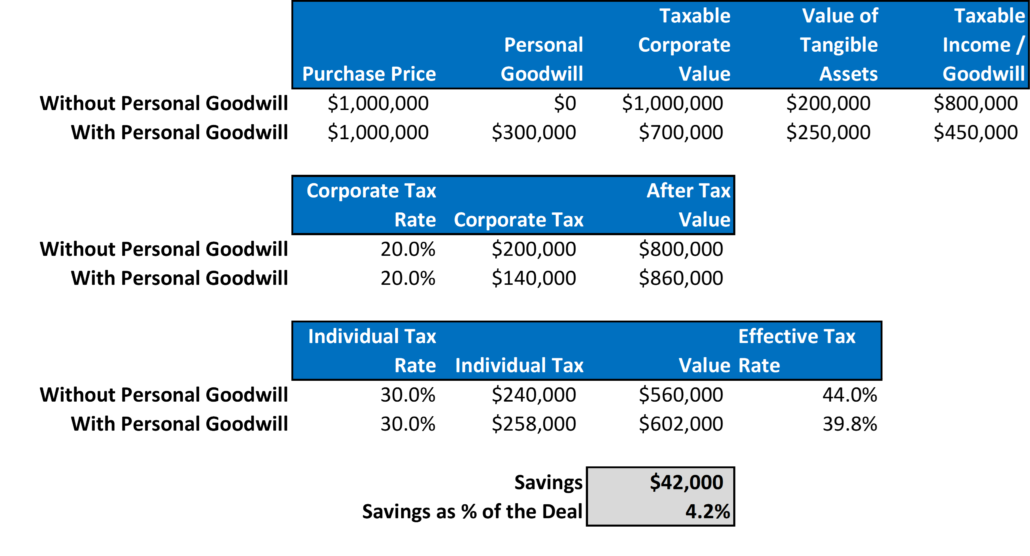

It is important to note that there must be a balanced relationship between personal goodwill to total goodwill. According to David Wood[5], personal goodwill should fall within 20%-to-40%. This range is supported by the tax court rulings and guides the appraiser in reconciling the analysis. While there may be a strong case for a higher percentage, it goes without saying that any conclusion above this range may trigger audit concerns unless the appraiser has presented strong support for an outlying opinion. Below is a simple analysis and calculation of the potential tax savings.

[1] Business Valuation Resources, LLC. Personal Goodwill: A Current Survey of Definitions. Adam Manson and David Wood CPA/ABV, CVA.

[2] Wood, David. (2007). Goodwill Attributes: Assessing Utility. The Value Examiner.

[3] Wood, David. (2007). “MUM’s the Word”TM: A formal Method to Allocate Blue Sky Value in Divorce. Business Valuation Update.

[4] Under ASC 805; asset recognition criteria.

[5] Business Valuation in Divorce. Case Law Compendium. Third Edition. Business Valuation Resources, LLC.

Exit Strategies Group, Inc (ESGI)

At ESGI, we are a team of seasoned appraisers to help you with your valuation needs, either to estimate the fair value of personal goodwill or any other. Our business valuations are commonly used in estate, gift, and other tax filings, dispute resolution, expert witness and litigation support, and mergers and acquisitions transactions.