Business Valuation: Step one in the sale process.

If you are considering selling your business, I would like to let you in on an M&A (merger and acquisition) professional’s insight. I have been involved in initiating and managing M&A transactions for over 15 years and have handled deals representing over $250 million in transaction value. Those transactions ranged from $2.6 mm to $90 mm. In addition, I was on a team that helped an international client acquire a $2.6 billion industry rival back in 2000.

Whether $2.6 million or $2.6 billion, these successful transactions started with a business valuation. The sale or acquisition of a business is a multi-step process, and the first step in a successful transaction between a buyer and seller almost always begins with a professional business valuation. Steps that follow the valuation include, marketing the company, buyer due diligence, negotiating the deal, and the closing.

A business valuation is a critical step on both sides of the deal table. Normally, the seller will do the first valuation, to get an idea of their company’s market value and then decide upon a price range that would motivate them to sell. The seller will generally share their historical and projected financial information with a vetted buyer. The buyer can then apply their own specific investment requirements to the shared information. Both sides utilize their valuations to negotiate the deal.

In my experience, no matter the size of the deal, the first step in a successful M&A transaction is a business valuation.

For more information on business valuation for M&A transactions, Email Louis Cionci or call him at 707-778-2040.

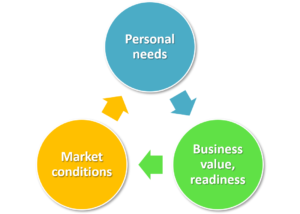

Going to market when you and your business are ready to sell and market conditions are right provides the best opportunity to maximize results. Let’s look at how these three ingredients combine:

Going to market when you and your business are ready to sell and market conditions are right provides the best opportunity to maximize results. Let’s look at how these three ingredients combine: Most business acquisitions by private equity firms have been “add-on” deals lately.

Most business acquisitions by private equity firms have been “add-on” deals lately.