Increase Business Value with Agreements

I recently completed an exit planning valuation of a business that enjoyed a very favorable discount on purchases of a key component used in the assembly of its products. The discount, negotiated many years ago, was a handshake deal between the founder of the company and his former employer who manufactured the component. This large discount enables the business to be significantly more profitable that it would be otherwise. Any investor or buyer for this business will naturally be concerned about whether the company can continue buying this component at the same below-market price.

I recently completed an exit planning valuation of a business that enjoyed a very favorable discount on purchases of a key component used in the assembly of its products. The discount, negotiated many years ago, was a handshake deal between the founder of the company and his former employer who manufactured the component. This large discount enables the business to be significantly more profitable that it would be otherwise. Any investor or buyer for this business will naturally be concerned about whether the company can continue buying this component at the same below-market price.We advised the business owner that before putting the business on the market, he try to secure a long-term contract with the vendor at the favorable discount, or attempt to find an alternate supplier of a comparable component at a similar price. If successful, his business will have substantially higher value and will attract more potential buyers when he goes to market.

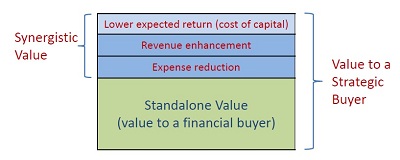

Agreements, properly structured, can increase enterprise value by reducing risk for buyers and shareholders.

Agreements to Have in Place Before Selling a Business

- Facility lease

- Client contract

- Construction contract

- Equipment lease

- Supplier contracts

- Distribution agreement

- Employment agreement

- Independent contractor agreement

- Non-competition agreement

- Collective bargaining agreement

- Financing of various kinds

- License or royalty agreement

- Franchise agreement

- Advertising agreement

- Joint venture agreement

- Others specific to your business

As part of an exit plan, business owners should examine all of their company’s third-party agreements, whether written or verbal, for things such as clarity, economic terms at market or better, contract term, exclusivity, transferability, legal validity and more. Involve competent legal counsel in all but the most routine business arrangements.

For advice on selling your company, preparing it to sell, or understanding its value and transfer-ability, call Jim Leonhard at 916-800-2716 or Email jhleonhard@exitstrategiesgroup.com.

Our seller and business valuation clients are usually proud of their company’s long-term relationships with major clients, and with good reason. Having a high percentage of business with a few customers can be a very profitable and personally satisfying way to run a business. It allows management to focus its attention and fine tune company operations to deliver exceptional service in a very cost-efficient manner. Customer acquisition expenses (marketing, sales, estimating, etc.) can be greatly curtailed or eliminated. It’s wonderful while it lasts.

Our seller and business valuation clients are usually proud of their company’s long-term relationships with major clients, and with good reason. Having a high percentage of business with a few customers can be a very profitable and personally satisfying way to run a business. It allows management to focus its attention and fine tune company operations to deliver exceptional service in a very cost-efficient manner. Customer acquisition expenses (marketing, sales, estimating, etc.) can be greatly curtailed or eliminated. It’s wonderful while it lasts.

A new

A new