How Discounts for Lack of Control are Determined

I recently penned a summary on valuation discounts for lack of marketability. As a follow-up, this post is about the other common valuation discount, the discount for lack of control (DLOC), which is often used when valuing minority interests in operating businesses.

I recently penned a summary on valuation discounts for lack of marketability. As a follow-up, this post is about the other common valuation discount, the discount for lack of control (DLOC), which is often used when valuing minority interests in operating businesses.

In the business valuation context, control refers to the ability to manage or control a business. A controlling shareholder enjoys many benefits that are not enjoyed by minority interest holders. Minority interests are therefore usually worth less, often a lot less, on a per share basis.

Control Premiums

Conversely, a controlling interest in a company is more valuable than a non-controlling interest because the interest holder can control policy, strategic and operational aspects of the company. An investor will generally pay more per share for the rights and liberties afforded a controlling interest than for a non-controlling interest.

When a control premium is warranted, the size of the premium is often based on the controlling interest holder’s ability to:

- Appoint or change members of the board of directors

- Appoint management

- Set management compensation and perquisites

- Set operational and strategic policy and change the course of the business

- Acquire, lease or liquidate business assets

- Negotiate and consummate mergers, acquisitions and divestitures

- Sell, liquidate, dissolve or recapitalize the company

- Sell or acquire treasury shares

- Register the company’s debt/equity for an initial or secondary public offering

- Declare and pay cash dividends to shareholders

- Change the articles of incorporation or bylaws of the company

- Establish, revise or execute buy-sell agreements

- Select joint venture partners or enter into such agreements

- Decide product/service offerings, pricing, and markets to serve and not serve

- Select suppliers, vendors and contractors to do business with

- Enter into license or technology sharing agreements regarding intellectual property

- Block any (or all) of the above actions

Evidence of Control Premiums in the Marketplace

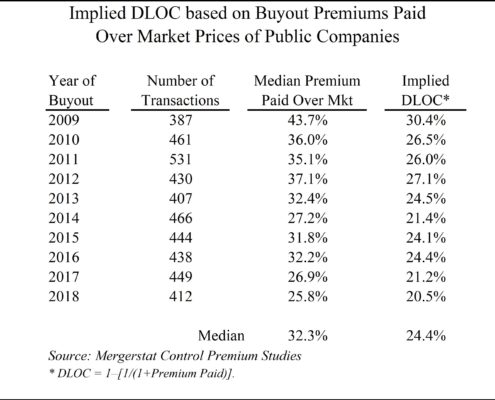

A variety of studies have examined the premiums paid when public companies are bought out. One such source is the Mergerstat Control Premium Study. Mergerstat calculates buyout price premiums paid over market prices five business days prior to public announcement of the buyout.

We compiled the following table from Mergerstat Control Premium Study data:

It is impossible to know exactly how much of the premiums paid were due to gaining control versus the existence of synergistic benefits between the acquirer and the acquired. Some business appraisers argue that a significant portion of the premium relates to synergies (or other non-control factors), while others accept these studies at face value.

Lack of Control Discounts

When a valuation method result is on a controlling basis and we are valuing a non-controlling interest, a Discount for Lack of Control is usually applied. DLOC’s cannot be observed directly in the marketplace. Instead they are calculated from control premiums:

DLOC = 1 – (1 / (1 + Control Premium))

Business appraisers often select a baseline DLOC from studies of empirical data, then adjust up or down to fit the specific control attributes of the interest being valued. Key items to consider when evaluating a minority interest for a DLOC include the non-controlling interest holder’s inability to take the actions listed above, as well as other power attributes of the subject interest and economic attributes of the company.

How the IRS and Courts See Control Discounts

The IRS, valuation professionals and the courts recognize the appropriateness of DLOC’s. In a 1982 estate tax decision (Estate of Woodbury G. Andrews, 79 T.C. 938) the court distinguished this discount from a discount for lack of marketability, stating in part, “The minority shareholder discount is designed to reflect the decreased value of shares that do not convey control of a closely-held corporation.” The tax court continued in Harwood v. Commissioner, 82 T.C. 239, 267 (1984), “The minority discount is recognized because the holder of a minority interest lacks control over corporate policy, cannot direct the payment of dividends, and cannot compel a liquidation of corporate assets.”

In establishing a DLOC, IRS Revenue Ruling 93-12 should also be considered if the interest being transferred results in a control block of shares among family members in the subject entity. In brief, this ruling states that a minority discount will not be disallowed solely because a transferred interest, when aggregated with interest held by family members, would form a controlling interest.

Exceptions to the Rules

Users of business valuations should be aware that some valuation methods produce a non-controlling level of value, and no adjustment is needed when the subject being valued is a non-controlling interest (sometimes referred to as a minority interest, although they are not always the same). For the business valuation expert, it is critical to identify the level of control implied in a valuation method result before applying a DLOC. In some cases, a valuation method generates the same level of value needed for the valuation assignment, and no discount is required. In other cases, the levels don’t match.

It should also be noted that a minority interest usually does not have the benefit of control; however there are situations where a minority interest has control, such as an organization that has shareholders with limited voting rights. A minority owner without special rights cannot control the paying of dividends or selling of assets, or otherwise direct or manage a company’s activities.

Exit Strategies Group values control and minority (non-controlling) interests of private businesses for tax, financial reporting, strategic, buy-sell, ESOP and other purposes. If you’d like help in this regard or have any related questions, contact Joe Orlando, ASA, at 503-925-5510 or jorlando@exitstrategiesgroup.com.