Exploring Donor-Advised Funds for Privately Held Business Owners’ Philanthropy

For business owners of privately held companies seeking a seamless and impactful way to contribute to charitable causes, Donor-Advised Funds (DAFs) have emerged as a philanthropic and tax-efficient solution. These vehicles offer a flexible and tax-efficient way to manage charitable donations, allowing donors to make contributions to a fund and then recommend grants to their favorite charities over time. Many people have successfully used DAFs to support the causes they care about, and there are numerous success stories available online.

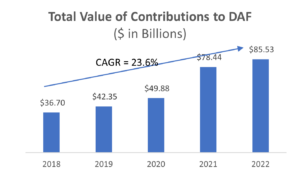

According to the 2023 DAF report, contributions to DAFs reached an all-time high of $85.53 billion in 2022. These contributions have grown at a double-digit compound annual growth rate (CAGR) over the last five years, as detailed below.

Source: National Philanthropic Trust. 2023 Donor-Advised Fund Report

Even though DAFs are an effective tax-efficient vehicle to make contributions, special attention, and professional advice are required to obtain such tax benefits and contribute to a good cause. (NOTE: Exit Strategies does not provide tax advice but will work with your tax advisors to help value the assets contributed to a DAF.)

Contributions of Private Securities

Most of the valuations we perform for the transfer of equity to DAFs are associated with the transfer of private equity securities. These transfers into DAFs frequently occur immediately before a pre-arranged stock sale.

In these situations, the donor hopes to claim a charitable deduction for the full fair market value of the gifted stock. However, because the sale of private securities always has risk, a qualified appraiser must pay special attention to discounts associated with a lack of liquidity (or a lack of control and marketability) that lowers the value of the donation to the Fair Market Value at the date of the gift rather than the anticipated timing of the income to the DAF. The appraiser must analyze related documentation of the donation, such as the private company’s by-laws, an operating agreement, or a buy-sell agreement, to see if there are any transfer restrictions in support of these discounts.

Form 8283

The IRS requires Form 8283[1] to be filed with a tax return in support of the resulting tax deduction for the donor. This form needs to be signed by the donor and the recipient, as well as the certified appraiser, along with a thorough, USPAP-compliant report required by the IRS for their review.

IRS-Compliant Report

The IRS considers several factors while reviewing a business valuation report, including the completeness of the report, whether it adequately discloses the methodologies applied, and the information necessary for a reader to understand the report. The IRS assesses whether the appraiser possesses the necessary skills and credentials to conduct the business valuation.

If you are planning to contribute private equity or other illiquid assets to a DAF, professional advice and planning is critical. A team of advisors, including a tax attorney and your accountant, will help you navigate this process. ESGI would welcome the opportunity to be part of that team as the valuation expert who opines on the value of these donations. Our team of appraisers includes professionals with the ASA designation (an Accredited Senior Appraiser) issued by the American Society of Appraisers[2], and our opinions meet strict IRS requirements and have been successfully defended in IRS review.

Exit Strategies has certified appraisers who value control and minority ownership interests of private businesses for tax, financial reporting, and strategic purposes. If you’d like help in this regard or have any related questions, you can reach Joe Orlando, ASA, at 503-925-5510 or jorlando@exitstrategiesgroup.com.

[1] https://www.irs.gov/pub/irs-pdf/f8283.pdf

[2] https://www.appraisers.org/credentials/business-valuation